Mortgages are big commitments.

The average one takes 25 years to pay off.

But things can change, and between 18,000 and 2,000 homes are foreclosed annually in the UK.

So, can you sell a foreclosed home?

Let’s find out.

Foreclosed home: Definition

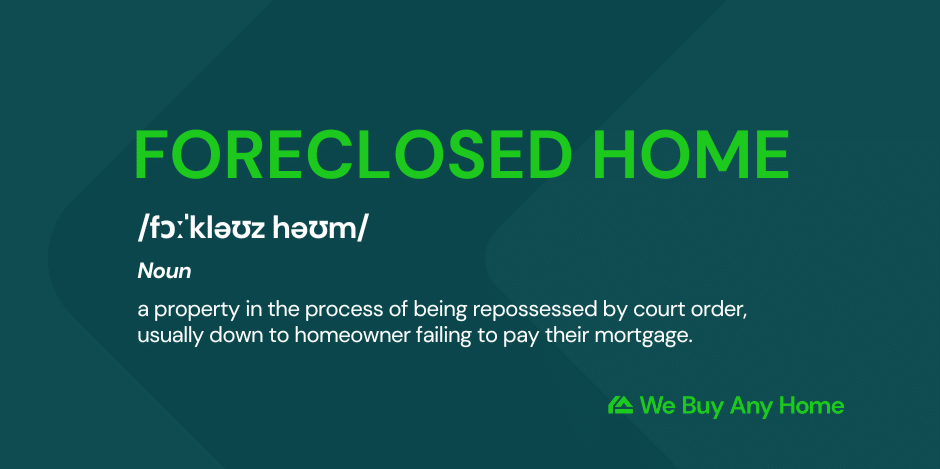

A home becomes foreclosed when it is in the process of being repossessed by a mortgage lender.

This usually happens following a court order, which lenders can get if the homeowner fails to repay their mortgage.

It could also be prompted by the homeowner breaching other mortgage agreement terms.

The lender can sell the property or keep it as an asset. It’s entirely up to them.

If a home is foreclosed, you can find this through public records. It might also look unkempt if no one has lived there or looked after it for a while.

Who owns a foreclosed home?

The lender owns a foreclosed home.

Borrowers may be able to renegotiate with them. However, this is rare when the foreclosure stage has been reached.

Selling a foreclosed home

Foreclosed homes can be sold by the bank or lender who now owns it.

Selling is often the quickest way for them to recoup the money they have lent for the house.

Foreclosed homes are usually sold via an estate agent or at a property auction.

In the former example, the bank can choose the price it lists the house for, but the property typically sells below market value.

This route is popular if it’s in terrible condition and they don’t have the time or means to fix it up.

Selling at auction provides funds from the sale quickly. This may be important for the bank’s cash flow.

Foreclosed homes selling prices

The bank can decide how much it sells a foreclosed home for. It’s entirely up to them.

Most lenders aim to sell quickly to recoup their losses.

It could be listed for around 15% below the usual market value in this case. And if it’s sold at auction, a 20% reduction in price is more common.

So, if a house is usually valued at £500,000, the bank may list it at around £425,000 or £450,000 on the open market. Meanwhile, £375,000 might be more typical when selling at auction.

Each circumstance is different and depends on:

- The house’s condition

- How much of a loss the bank takes

- How urgently the bank needs short-term cash flow.

Stop the sale of a foreclosed home

When a lender forecloses on your house, they become the legal owner. This means they have the right to sell your property.

There are a couple of things you can try to prevent the sale. But there’s no guarantee these will work.

To start with, you could negotiate with the lender. This might involve a clearly outlined payment plan.

However, they’re unlikely to be receptive to this if it’s already reached the point of foreclosure.

Sometimes, filing for bankruptcy can temporarily stop the foreclosure process. But you should never do this without consulting a professional accountant or lawyer.

There are severe wider repercussions for declaring bankruptcy. These include increasing the difficulty of getting a mortgage in the near future.