Borrowing against your home is a strategy that sounds sophisticated and clever. After all, if you’ve got a house worth hundreds of thousands, it seems a waste not to put it to good use. If you can use it to unlock extra money (albeit in the form of a loan) then that makes perfect sense – right?

Unfortunately, this theory doesn’t always shape up. For one thing, you’re always increasing the debt you’re in when you borrow against your home. And the stakes are also much higher – because if you fall behind on payments, you lose your house.

We’re not saying that borrowing against your house never makes sense. In specific cases, it could be a useful tool. However, for every success story about someone who leveraged their house into riches, there are far more quiet disasters. The kind people don’t like to talk about. So, it’s time we gave you the honest truth.

What does ‘borrowing against your home’ really mean?

You might’ve heard the phrase before, but that doesn’t mean you know what it means. Don’t worry, because we’re about to sort that out.

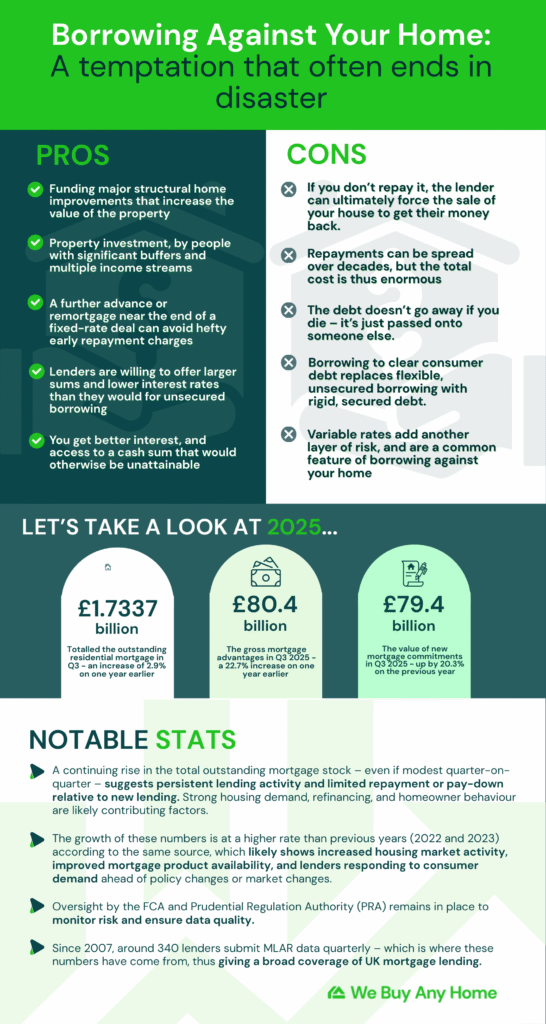

At its most basic level, borrowing against your home means using your property as security for a loan. If you don’t repay it, the lender can ultimately force the sale of your house to get their money back. That’s the deal you sign.

In the UK, this usually happens through a remortgage, a further advance from your existing lender, or a secured loan. The names differ, but the risk is usually the same. Each one might be slightly more preferable in different circumstances, which an adviser can guide you on. In some cases, more complex structures are used, such as a Joint Borrower Sole Proprietor mortgage, which allows additional income to support borrowing without shared ownership.

Because property is valuable, lenders are willing to offer larger sums and lower interest rates than they would for unsecured borrowing. That’s what makes it attractive. You get better interest and access to a cash sum that would otherwise be unattainable. But the risks are huge, and with so many alternatives out there, it’s almost never worth it.

Lower monthly payments don’t mean lower risk. They often mean longer terms, bigger total costs, and far less flexibility if something goes wrong.

Why borrowing against your house sounds like a great idea

The appeal is obvious to anyone who’s asset-rich but cash-poor. The equity in your home feels like money that’s already yours, but ‘trapped’, and you want to free it so it can be put to better use.

Unfortunately, the way this opportunity may ‘look’ at first glance isn’t reflective of reality. Repayments can be spread over decades, but the total cost is enormous, and it doesn’t go away if you pass away – it’s just passed onto someone else. The monthly figure might look manageable, but the lifetime one is not.

There’s also a powerful psychological trick at play. Borrowing against your home doesn’t feel like ‘real’ borrowing, in the same way a credit card does, because it feels like moving money from one pocket to another.

That’s where lots of people get caught out. You’re not rearranging money you already have. You’re taking on new debt with very serious consequences.

‘Affordable’ is not the same as ‘safe’

If you think that ‘affordable’ and ‘safe’ mean the same thing, then you’ve fallen into a classic trap of borrowing against your home.

Most of these loans run for years, and often decades, which means that over that time, lots can change. Major economic changes, such as interest rate rises or new government policies, can turn your situation upside down.

Variable rates add another layer of risk and are a common feature of borrowing against your home. Monthly payments can look reasonable at the current rates – but as soon as these interest rates go up, you’re in trouble.

The main reasons people borrow against their home

Despite all the negatives listed further above, people do still decide to borrow against their home. With the right advice and understanding of all the consequences, it can occasionally work. Just make sure you have your eyes wide open going into it.

In theory, borrowing against your house is meant to be strategic. But, in reality, it’s typically driven by impatience.

Often, changing spending habits can be difficult, and borrowing against your home can feel like a ‘get out of jail free’ card, especially if it’s sold to you in a certain way.

Making an investment is also more attractive than playing the waiting game. Homeowners can at their equity and view it as ‘wasted money’. Why wait several years (until you sell) for it to become useful, if you can put it to good use today?

Sometimes that works, but often, it doesn’t. Buy-to-let margins have been squeezed by tax changes, higher mortgage rates, and tighter regulation. Many hopeful investors have discovered that property is not always a certain win.

Debt consolidation is another big driver. Turning high-interest unsecured debt into lower-interest secured debt feels sensible. It often, however, just moves the problem rather than solving it; if you’re considering this route, it’s important to understand exactly how debt consolidation loans work before securing them against your home. Kicking the can down the street does not mean that the issue goes away. The debt also becomes larger in the process. Many homeowners consider remortgaging to clear debt, but whether that’s wise depends heavily on your situation.

Then there’s borrowing to fund a business. While it’s good to believe in yourself, it’s a huge commercial risk, with an enormous percentage of start-ups failing within the first 12 months. If you’ve got a family or an expensive lifestyle, you’re putting it all on the line.

Examples when borrowing against your home could make sense

If you ask any financial adviser, they’ll tell you: it’s not all doom and gloom, and there are a few cases when borrowing against your home makes perfect sense. If you approach it with a realistic view of risk, along with lots of planning, then it could go well.

One example is funding major structural home improvements that genuinely increase the value of the property. Make sure that the increase in value is indisputable, such as increasing square footage or fixing serious issues. Even then, the numbers must be conservative. Overestimating value uplift is a classic and costly mistake.

Another is experienced property investment, usually by people with significant buffers and multiple income streams. Even among professionals, opinions are divided on whether this is a wise move. It’s not something that translates well to average households.

There are also technical cases where a further advance or remortgage makes sense near the end of a fixed-rate deal, particularly if it avoids hefty early repayment charges. That’s less about ambition and more about damage control.

The common thread in all these cases is that you understand the risks.

Why it’s a bad move in most ‘typical’ situations

For most people, borrowing against your home is an unnecessary escalation of risk.

One of the worst reasons to do this is to pay for a better lifestyle. Turning short-term pleasure into long-term obligation is never a good trade. And, even if you’re nearing the latter years of your life, it’s a debt that’ll be passed on to all your loved ones when you pass away.

Borrowing to clear consumer debt is another bad idea, in most cases. It replaces flexible, unsecured borrowing with rigid, secured debt. If something goes wrong, the consequences are far more severe.

Timing also matters. Borrowing heavily during periods of economic uncertainty is particularly risky. Sometimes there’s an economic nightmare around the corner, without it being possible for you to know this. That’s why exercising caution is always the best way to go.

Are failures underreported?

Many economists and financial experts argue that the reason borrowing against your home remains popular is that failures are underreported.

People talk about wins and tend to advertise them in a very public setting. But you’re far less likely to come across a public post about why it worked out terribly for someone. No one likes to broadcast their mishaps!

Forced sales don’t happen overnight – they’re the end of a long chain of events. Indeed, some people don’t even put all the pieces together when their financial situation worsens and fail to recognise that that’s where the problems began.

Even when repossession doesn’t occur, the psychological toll can be heavy. Living with the knowledge that your home is directly tied to financial performance puts a huge pressure on your shoulders, which most people could do without.

There’s a key factor missing from your spreadsheet…

When you sit down to consider the pros and cons of borrowing against your house, you’ll probably put a spreadsheet together. But, there’s a key factor that won’t be found on a spreadsheet – and it’s probably the most important one of all.

Emotional challenges.

Financial advice often focuses on numbers, without factoring in the emotional cost. Not only is it hard to quantify, but each person deals with these situations differently.

A secure home provides stability that goes far beyond money. You may not even notice the peace of mind on a daily basis, because you take it for granted. But trust us – when you don’t have that comfort, you’ll feel it straight away.

What are the alternatives?

Before borrowing against your home, it’s crucial that you explore all the other options.

Unsecured borrowing may look more expensive, but it doesn’t put your house at risk. This is a worthwhile trade-off in many cases.

There are other ways to improve your finances, such as selling assets, delaying plans, or changing your spending habits. These are practical steps, which cost far left, and improve your position rather than worsening it.

In debt situations, behaviour matters more than interest rates. Refinancing without reforming habits is a waste of everyone’s time.

Independent advice is crucial. Mortgage brokers, financial advisers and debt charities can provide perspectives that aren’t tied to selling you a product. It’s a good idea to discuss with these individuals. After all, if it’s a good idea, then it can stand up to scrutiny.

Borrowing against your house – within the context of the UK market

Each country’s economy is different, including cultural approaches to debt and the acceptability of risk.

UK homeowners already carry significant mortgage debt due to the cost of living pressures and the ever-rising gap between average income and house value. So, you’re already starting in a tricky position.

Housing markets change, and the UK is not immune to this pattern (despite what people tell you). If property values fall while you’ve increased borrowing, you could find yourself in negative equity, a situation every homeowner should understand before leveraging their home. What looks sensible in one situation can become dangerous in another. Borrowing against your home limits your ability to adapt.

Flexibility is underrated. Once your house is heavily leveraged, your options narrow quickly, and you can feel stuck.

Borrowing against your home is not always reckless – just do your homework!

Borrowing against your home is not automatically a bad idea. However, it is rarely as safe as it’s made to sound, especially when you factor in all the alternative solutions that’re out there.

For most people, it’s a solution that creates more problems than it solves, and trades long-term security for short-term progress.

If you’re considering borrowing against your house, that alone should be a signal to slow down, seek independent advice and ask uncomfortable questions about what could go wrong. Once you’ve made the jump, you can’t take it back, so it’s an excellent idea to move cautiously.

Your home is more than an asset. It’s your safety net, your place to relax, and the foundation for an exciting future. Treating it like ‘just another financial tool’ is a gamble that shouldn’t be taken without serious consideration.