In 2013 nearly 7,000 mortgage repossession claims were issued in London alone, and 1.75 per cent of all mortgages in the UK were in arrears. If you fall behind on your mortgage payments, there is a risk that your home could be used as collateral to be sold by your mortgage lender, or a third-party seller to recoup the outstanding money. This can be a very stressful process and one that can easily spiral out of control. However, this does not have to be the case, the process is open to reasonable negotiation and a number of preventative measures can be taken to halt the repossession of your home.

It is also worthwhile remembering that a court must consider both the interests of the financial institution in terms of operating a profitable business and the homeowner’s need for shelter. The whole process is tailored to avoid a ‘breach of peace’, so it is important to get your ducks in a row with regards to documentation and plans going forward.

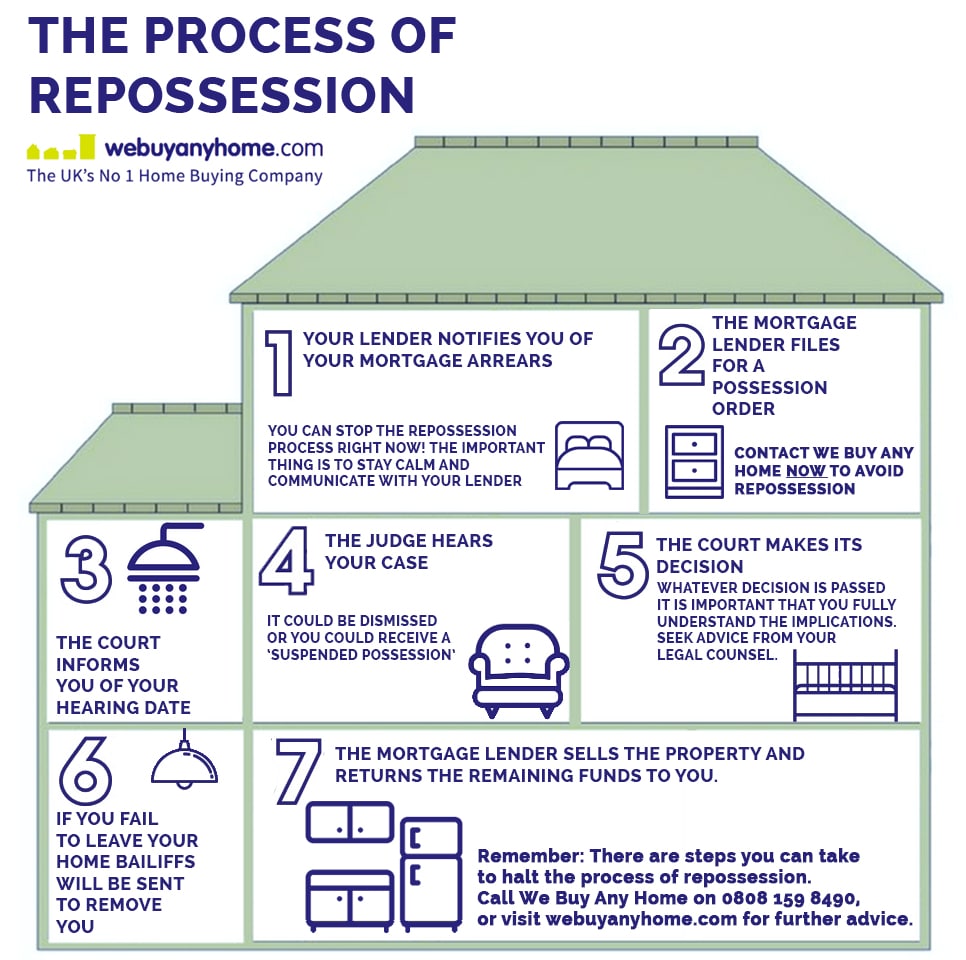

Home Repossession Process

This step-by-step guide to the legal process of repossession should help you to consider what actions to take at each step, and how to avoid the loss of your property. After all, everyone should be able to have the option of when and how to sell their home.

- You receive notification from your lender about your mortgage arrears

- They should contact you to request you find a solution; this gives you a chance to put together a proposal for your lender. This could include any of the following:

- Changing to an interest-only mortgage to reduce the monthly cost

- Adding your arrears to the mortgage itself

- Taking a ‘mortgage holiday’ (if your mortgage is flexible)

- Selling an endowment policy

- At this stage, you could also consider acting to raise the required funds to pay your lender. You could:

- Take in a lodger

- Rent out your home

- Put your home on the market yourself

- The lender then accepts or declines your solution; if they decline then they will warn of court action to begin repossession.

REMEMBER: There are plenty of services and options available today to streamline the process of renting or selling your home. Finding a lodger may be particularly suitable if you require income stability for only the next 6 months to a year, i.e. if you are on maternity leave, in between jobs or recovering from an illness. If it seems that you will not be able to come up with the necessary funds after a year has elapsed then perhaps it is worth considering a sell house fast route, especially if the alternatives are merely stop-gap measures. In time sensitive situations such as this, this may be a wise route and saves you the potential distress and work involved in going to court.

- The mortgage lender proceeds with filing a suit in court asking for a possession order

- The court will write to you to inform you of the hearing date

- At this stage, you must complete and return the included defence form

- You should also seek legal advice in preparation for the hearing, in most cases, a free ‘lay representative’ would provide a possible solution

- The case is taken to court and the judge hears the repossession case

- The outcomes from this include;

- your home being repossessed and the lender selling the property to pay your dates

- A suspended possession order is made meaning you can stay in your home under certain repayment conditions.

- The judge may also choose to postpone or dismiss the case.

- If the court has made an order for repossession:

- You generally have between 28-56 days to leave your home.

- Usually, lenders will add their legal costs to your outstanding payments.

- If you fail to leave your home in the specified time, Bailiffs will be sent to remove you.

- Bailiffs need a warrant to remove you and will provide a set eviction date. They cannot use violence, nor the threat of violence, but are able to call the police should you resist eviction.

- The cost of the Bailiffs is commonly added to the outstanding debt.

- The mortgage lender sells your home

- Until this sale is complete you must continue to pay the interest on what you owe. Any leftover funds from the sale will be transferred to you.

- If there is any shortfall then this will have to be paid separately, through agreed and negotiated terms with your mortgage lender.

- Any residing debt after the sale may also be transferred to whomever the property was sold; you will then own this party. Likewise, insurance may cover the shortfall payment to the mortgage lenders; you will then owe this to the insurance company.

REMEMBER: The mortgage lender must keep all communications with you clear and easy to understand. If at any point you become confused it is important that you seek clarification and take every opportunity to understand their argument and requests so that you can best form your defence position.